📄 Detailed Analysis: Statement of Financial Transaction (SFT) Return

Overview

Introduction

Accumulation of black money has been one of the major threats to the Indian economy. The government of India along with the ministry of finance has been striving towards curbing black money and also widening the tax base and has taken numerous initiatives in this regard.

One such initiative was to cast an obligation on government agencies and other authorities who are a valuable and reliable source of information, to report high-value transactions. Such specified persons were required to submit ‘Annual Information Return (AIR)’ introduced in 2003 with respect to specified financial transactions under Section 285BA.

Later, Finance Act 2014 replaced Section 285BA and renamed it as ‘obligation to furnish statement of financial transaction or reportable account’ to widen the scope of specified persons and to introduce various other provisions.

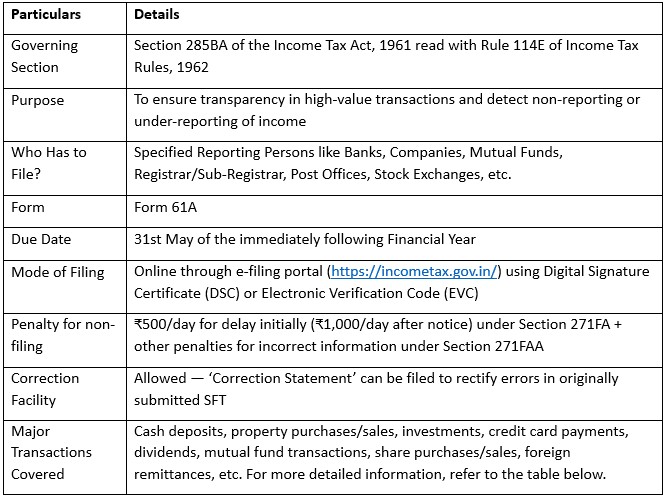

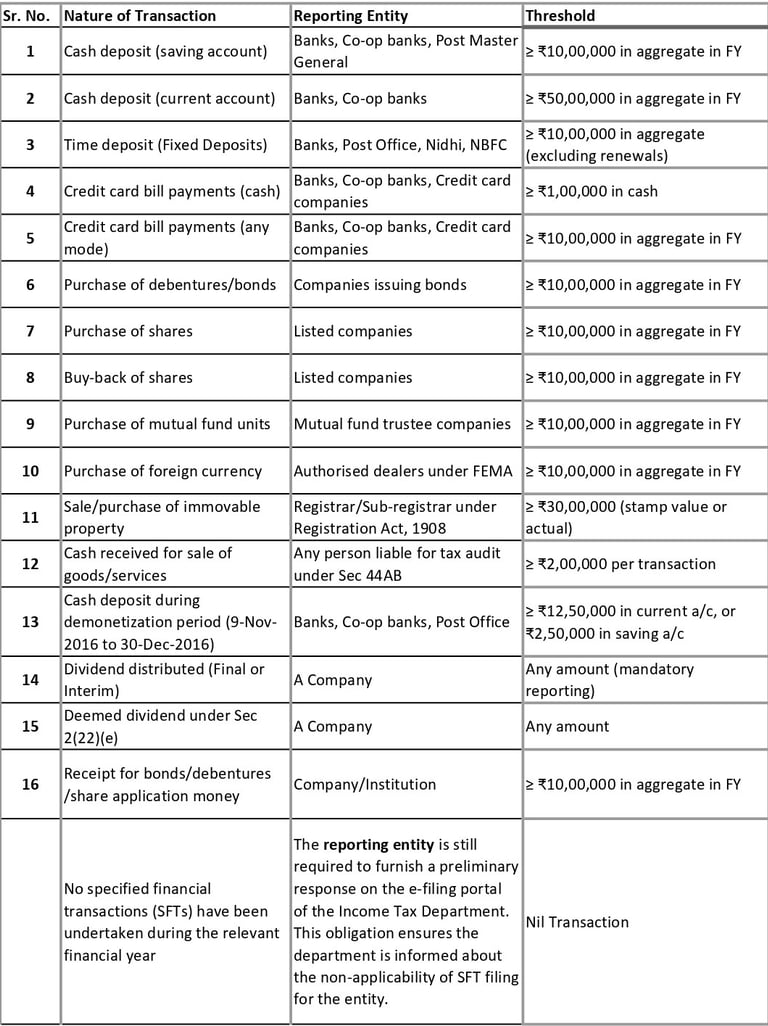

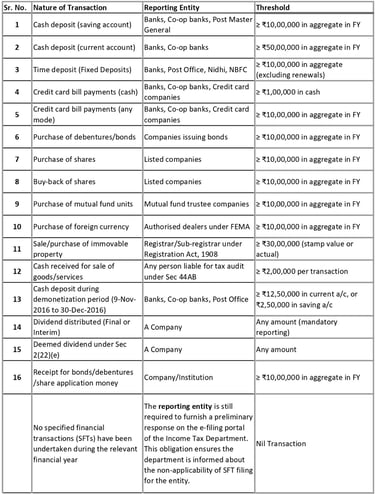

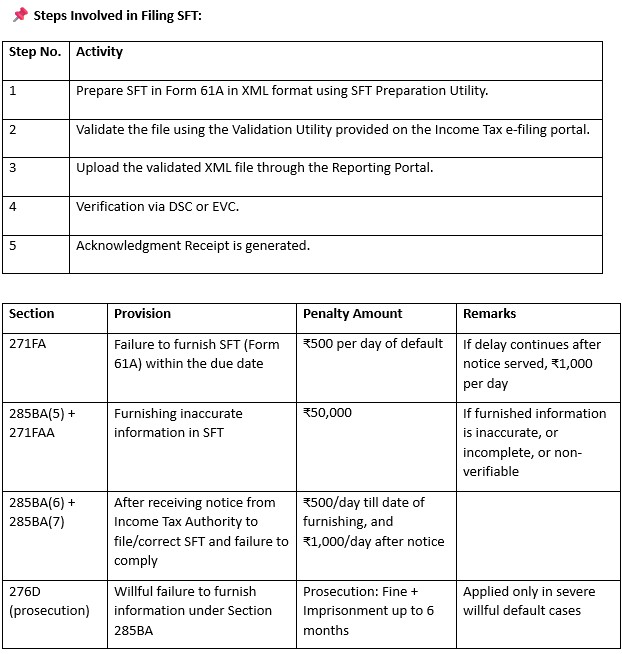

The Statement of Financial Transaction (SFT) is a reporting mechanism requiring certain entities to submit details of significant financial transactions to the Income Tax Department. Governed by Section 285BA and Rule 114E, SFT is filed annually using Form 61A by May 31 of the following financial year. Transactions involving listed securities and mutual fund units are reported semi-annually.

Transactions Reported in SFT

SFT covers the following transactions:

High-value financial transactions

Dividend payments

Interest payments

Transactions in listed securities and mutual fund units